Trading Day vs Calendar Day: Which to Use?

A clear comparison of trading days vs calendar days—definitions, a use-case decision map for performance/risk/operations/fees, a pros-and-cons table, and edge cases (time zones, holidays, corporate actions, 24/7 markets) to help you choose the right day count fast.

Trading Day vs Calendar Day: Which to Use?

A clear comparison of trading days vs calendar days—definitions, a use-case decision map for performance/risk/operations/fees, a pros-and-cons table, and edge cases (time zones, holidays, corporate actions, 24/7 markets) to help you choose the right day count fast.

Ever had a return report, SLA, or fee accrual “miss” simply because two teams counted days differently? Trading days and calendar days sound interchangeable until a weekend, holiday, or market cutoff shows up and the numbers stop matching.

This comparison gives you a practical way to decide which day count to use in each situation. You’ll get plain-language definitions, a decision map by use case, the gotchas that cause disputes, and a quick rubric so you can standardize your choice with confidence.

Define the days

Trading days and calendar days measure time in different worlds. One follows market sessions, the other follows the clock. Pick the wrong one and your timeline, risk window, and expectations drift fast.

Trading day meaning

A trading day is a day your market is actually open for the instrument you trade. That excludes weekends, full holidays, and sometimes includes shortened sessions or venue-specific hours.

A U.S. stock trading day can differ from a futures trading day, even on the same date. Some products trade nearly around the clock, then pause for maintenance or a brief close. Your broker’s definition usually follows the primary listing exchange or the product’s session calendar.

Treat “trading days” as a schedule, not a date range.

Calendar day meaning

A calendar day is any consecutive day on the calendar, regardless of market hours. Weekends, holidays, and overnight time all count.

Calendar days match real-world deadlines like contracts, notices, margin call clocks, and “by Friday” obligations. They also match how you experience risk when markets are closed but news still happens.

If the world can change, the calendar is still running.

Where confusion happens

Most confusion comes from mixing a market schedule with a real-world clock. The tricky parts show up in these spots:

- Settlement cycles: trading days vs banking days

- Performance windows: 5 trading days vs 7 days

- Interest accrual: daily interest despite closure

- Reporting dates: as-of date vs publish date

- Corporate actions: record date vs payable date

When you see a number and a unit, confirm which clock you’re on.

Use-case decision map

Day-count conventions are a coordination tool. Pick the convention that matches the mechanism creating the number, then document it. When something looks “off,” assume a mismatch and check the source document.

Performance measurement

Returns and risk metrics come from price changes. Prices move on trading days.

Use trading days when you’re doing any of these:

- Daily returns, weekly returns, and rolling windows

- Volatility, tracking error, and information ratio inputs

- Drawdowns and “days to recover” based on observed prices

Use calendar days when the question is about the investor’s clock:

- Month-end and quarter-end reporting packs

- Subscription and redemption cutoff cycles tied to dates

- “Since inception” periods defined by start and end dates

If your report is calendar-based but your math is trading-based, label both clocks explicitly.

Risk and models

Risk models compare horizons. Horizon definitions drift if you mix day types.

- Use trading days for volatility scaling from daily returns.

- Use trading days for backtests that rebalance on market sessions.

- Use calendar days for horizons defined as “10-day” by policy.

- Align VaR horizons with the model’s return frequency.

- Match benchmark and portfolio conventions in comparisons.

If two VaR numbers use different clocks, you’re not comparing risk. You’re comparing calendars.

Operations and deadlines

Operations run on dates and business days. Markets closing early does not move legal deadlines.

Calendar-based timelines usually include:

- Subscription and redemption notices

- Compliance filings and regulatory submissions

- Client communications and contractual deliverables

Reconcile closures by translating “X calendar days” into a cutover schedule:

- Identify non-business days for the relevant jurisdiction

- Pre-assign the effective processing day if the date lands on a closure

- Confirm the fund document’s “business day” definition

The trade blotter follows the exchange. Your obligations follow the document.

Fees and accruals

Fees accrue with conventions. Pricing moves with trading.

- Use calendar day-count fractions for management fee accruals, if specified.

- Use calendar conventions for interest accruals (e.g., ACT/360, 30/360).

- Use trading days for P&L attribution from price moves.

- Use contract terms for financing charges and reset schedules.

- Check holiday handling in ISDA-style definitions.

Accruals are contractual math. Don’t “annualize” them with a trading-day shortcut.

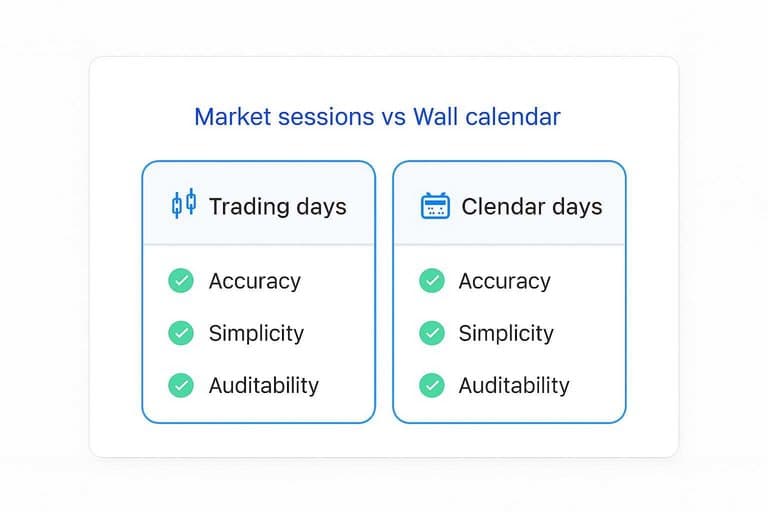

Pros and cons table

You’re choosing a clock for finance: market sessions or the wall calendar. Pick the one that matches how your metric is actually used—especially if your process is built around end-of-day market data.

| Dimension | Trading days (pros) | Calendar days (pros) | Where each bites you |

|---|---|---|---|

| Accuracy | Matches market exposure | Matches real time | Misstates decay or holding |

| Simplicity | Fits trading systems | Fits human planning | Adds conversion friction |

| Auditability | Aligns with broker logs | Aligns with invoices | Confuses mixed sources |

| Comparability | Standard for returns | Standard for projects | Skews cross-domain comparisons |

| Stakeholder expectations | Traders expect it | Executives expect it | Creates “why different” debates |

If you keep having to “explain the clock,” you picked the wrong one. For most swing-trading workflows (e.g., reviewing daily relative strength, breadth, and rotation after the close the way Open Swing Trading is designed for), trading days tend to be the more honest unit because they map to actual market sessions and decision points—whereas calendar days can quietly blur what was tradable versus what was just elapsed time.

Hidden edge cases

Most “day” debates break on the weird stuff, not the basics. When the contract or venue defines the clock, your preference stops mattering.

Time zones cutoffs

A “day” is often a cutoff time plus a time zone, not a sunrise-to-sunset idea. NAV strikes, end-of-day marks, and cross-border trading can move the effective boundary.

Imagine a fund that prices at 4:00 pm New York, while you trade in London. Your “same day” order can land in tomorrow’s NAV, even if markets were open.

If the cutoff is written down, treat it as law and build your logic around it.

Holiday calendars

Exchanges don’t share a single holiday calendar, and your portfolio inherits every closure. Mixed assets force you to pick which calendar controls each leg.

- Maintain a per-venue trading calendar

- Map each position to its primary venue

- Define a portfolio-level fallback calendar

- Gate rebalancing on the last open venue

- Record the calendar used in reports

The calendar choice is part of the result, so store it like you store prices.

Corporate actions

Corporate actions create “days” that behave differently for returns, eligibility, and settlement logic. Ex-dates and effective dates can slice your measurement window in ways your day-count convention won’t fix.

A split can make a calendar-day window look like a giant move, unless you adjust at the correct effective timestamp. An index rebalance can shift constituents overnight, changing what “the market” even was.

When actions are in play, anchor windows to event timestamps, not just day labels.

Crypto and 24/7

Crypto trades continuously, so “trading day” needs an artificial boundary. You usually pick a session definition, or a fixed UTC day, then stick to it.

- Use UTC 00:00–23:59 for reporting

- Use exchange session windows for execution

- Use funding-rate intervals for derivatives

- Use rolling 24-hour windows for risk

- Disclose the boundary in performance docs

Pick the boundary that matches your decision cycle, not your charting tool.

How to choose quickly

Pick a day convention fast, then lock it in. You’re avoiding mismatched lookbacks across dashboards, backtests, and stakeholder emails.

- Write the decision in one line: “We report in trading days” or “calendar days.”

- Map every input to that line: data sources, markets, time zones, and holidays.

- Convert the holdouts explicitly: calendar-to-trading via market calendar, or trading-to-calendar via date ranges.

- Add the convention to every chart and query: titles, footnotes, and parameter names.

- Create one crosswalk check: spot-test a window in two tools for the same period.

After that, any discrepancy is a data issue, not a definition fight.

Rubric and recommendation

Choosing trading days versus calendar days is a governance decision first, then a modeling choice. Pick the unit that matches the obligation you must satisfy, not the chart you prefer.

Selection checklist

Use this checklist to force clarity before you calculate anything. You are deciding what “one day” means for your decision.

- Define the purpose and decision context

- Identify the stakeholder and reporting audience

- Confirm instrument trading hours and holidays

- Match the data frequency and timestamp convention

- Read contract terms for day-count definitions

- Check regulatory rules and disclosures

- Test comparability across peers and periods

If you can’t answer three items cleanly, you don’t have a day unit yet.

Scoring rubric

Score both options, then choose the higher total for your use case. Keep the weights stable across projects.

| Criterion | Weight | Trading day score | Calendar day score |

|---|---|---|---|

| Accuracy to purpose | High | ||

| Consistency over time | Medium | ||

| Simplicity to explain | Medium | ||

| Compliance and documents | High |

When totals tie, let compliance win. Always.

Default recommendation

Use trading days for market behavior analysis, like returns, volatility, and event windows tied to sessions. Use calendar days for real-world obligations, like interest accrual, notice periods, lockups, and SLA clocks.

Override the default when governing documents define the day-count rule. That’s the line that gets crossed.

Make the Day Count Explicit (and Defensible)

If you only do one thing, define “day” in writing: the calendar, the time zone, the cutoff time, and whether weekends/holidays count. Use trading days for market-driven measurement (returns, volatility, backtests) and calendar days for real-world obligations (settlement-like deadlines, notices, contractual periods) unless a contract specifies otherwise. When in doubt, apply the rubric, pick a default, and document exceptions (holidays, corporate actions, 24/7 assets) so reports and decisions stay comparable.

Frequently Asked Questions

Do weekends and market holidays count as trading days when a broker says “T+1” or “T+2”?

No—T+1/T+2 settlement is counted in trading days, so weekends and market holidays don’t advance the clock. Always confirm the market’s holiday calendar and any special settlement rules for the asset (e.g., some mutual funds and OTC products differ).

How do I convert trading days to calendar days for a deadline or project plan?

Map the start date to the market’s official trading calendar, then count forward only open sessions to the target trading day and read off the resulting calendar date. If you need automation, use an exchange calendar (NYSE/Nasdaq) or a library like pandas_market_calendars to generate the trading sessions.

Is a “1-month” lookback the same as “21 trading days” for returns and volatility?

Not exactly—21 trading days is a fixed session count, while a calendar month varies in both days and holidays, which changes the sample length. For comparability across reports, pick one convention and label it explicitly (e.g., “21D” vs “1M”).

When reporting performance, should I annualize using 252 trading days or 365 calendar days?

Use 252 trading days when annualizing metrics based on daily market returns (volatility, Sharpe inputs), and 365 calendar days when the underlying process accrues every day (interest, fees, some carry). The key is matching the day-count to how the series is generated and documented.

How should I handle time zones and partial trading days when counting a trading day?

Anchor the “trading day” to the exchange session definition (local exchange time) and treat early closes or half-days as trading days unless your contract/spec explicitly excludes them. For cross-market workflows, normalize timestamps (e.g., to UTC) but keep session boundaries tied to each venue’s calendar.

Turn Trading Days Into Action

Once you’ve mapped trading days vs calendar days, the real edge comes from applying that choice consistently across your scans, backtests, and daily prep.

Open Swing Trading gives you daily-after-close RS rankings, breadth, and sector/theme rotation context across ~5,000 stocks so your “day count” decisions translate into better watchlists—get 7-day free access.